5 Things to Know About Zakat and Your Savings

Understand the essentials of Zakat on savings with our step-by-step guide tailored for the Singapore Muslim community. Learn what wealth is subject to Zakat, how to calculate it, exemptions, and its spiritual and communal benefits. This comprehensive guide equips you with actionable insights to fulfill your Zakat obligations confidently.

ISLAMIC FINANCEWEALTH MANAGEMENTZAKAT AND CHARITY

BeShariahWise

1/10/20256 min read

Introduction

Zakat, one of the five pillars of Islam, is an act of worship that purifies wealth and promotes community welfare. For Muslims, managing personal finances while fulfilling this obligation is crucial in aligning wealth with faith.

However, understanding how Zakat applies to our wealth, especially savings or acquired wealth, can sometimes be challenging.

Additionally, how does Zakat impact the rest of our financial portfolio, which includes modern financial systems like CPF and various investments?

This article outlines five critical aspects of Zakat and savings, focus primarily on the wealth that most people possess, tailored specifically for the Singapore Muslim community.

From calculating Zakat to understanding exemptions, this article provides actionable insights to help you fulfil your obligations with confidence and ease, InsyaAllah.

Fundamentals

Before going through the list, let us delve into the basics of Zakat itself.

Definition of Zakat

Zakat is an obligatory act of charity for Muslims who meet certain conditions. As a form of worship (Ibadah) related to wealth, the word ‘Zakat’ means growth, purification, and blessings.

This practice aims to purify wealth and help eradicate poverty in the community.

By redistributing wealth to the underprivileged, paying Zakat fosters generosity, love, and mutual help in society, while diminishing miserliness and greed.

Conditions of Paying Zakat

Zakat is obligatory for the following:

Every Muslim, including children. A guardian or next of kin should assist in fulfilling this obligation.

Individuals who have complete ownership of certain assets, with no restrictions on their use.

Wealth that meets or exceeds the Nisab, the minimum amount liable for Zakat.

Wealth that has been in the owner's possession for a complete lunar year (Haul).

Nisab

Nisab is the minimum threshold of wealth that makes one liable to pay Zakat.

For Zakat on currencies, the Nisab is based on 86 grams of gold, with its monetary value changing periodically.

If your savings drop below the Nisab threshold at any point, the Haul period is reset, and the calculation restarts once the savings reach the Nisab level again.

Haul

Haul refers to the period of one lunar (Hijri) year, approximately 355 days, during which wealth must be held liable for Zakat.

The Haul period begins when your savings first reach the Nisab or from the date of the last Zakat payment for recurring years.

If your savings fall below the Nisab at any point, the Haul period is broken, and a new Haul period begins when the savings once again meet or exceed the Nisab.

For Zakat on savings, it is calculated based on the lowest balance in the savings account(s) during this period.

1. What Kind of Wealth Is Subject to Zakat?

Not all forms of wealth are required to pay Zakat. Only specific types of wealth are liable for Zakat if they meet the requirements of Nisab (minimum threshold) and Haul (held for a lunar year). The following categories are usually included:

Cash Savings: This includes all money in your bank accounts, whether personal, joint, or business accounts.

Gold and Silver Holdings: Precious metals, whether in the form of jewellery (with certain conditions), coins, or bars, are subject to Zakat based on their current market value.

Investments: Profits or capital from Shariah-compliant investments, such as Islamic stocks, Sukuk, or unit trusts, are Zakat-able (Investments or proceeds from non-Shariah compliant financial products are not liable for Zakat as they are considered impermissible income and should be disposed of immediately).

2. How to Calculate Zakat on Savings

This article focuses on calculating Zakat on your savings held in bank savings or current accounts. The process is straightforward with a clear formula.

Zakat is calculated at 2.5% of the identified savings amount (the lowest savings amount of the entire lunar year) that exceeds the Nisab and has fulfilled the Haul period.

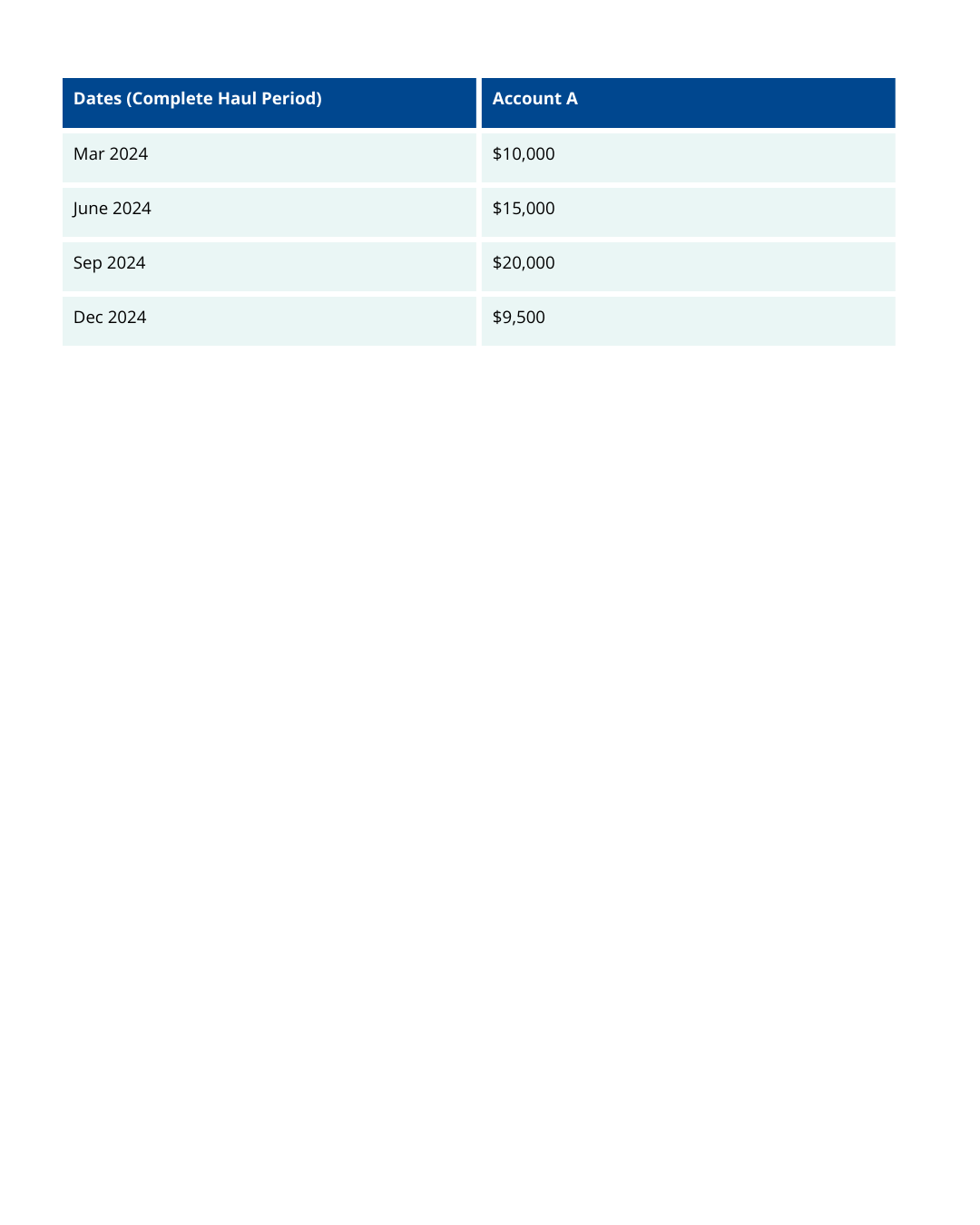

Step-by-Step Guide (Single Savings Account):

Determine the Nisab value in SGD for reference.

Identify the lowest balance within the Haul period (the previous 12 months).

Deduct any immediate debts or liabilities due within the same period (if any).

Multiply the remaining amount (lowest balance – debts) by 2.5%.

Example Calculation:

Lowest Balance: $9,500

Nisab: $9,000 (in Dec 2024)

Zakat Amount: $9,500 x 2.5% = $237.50

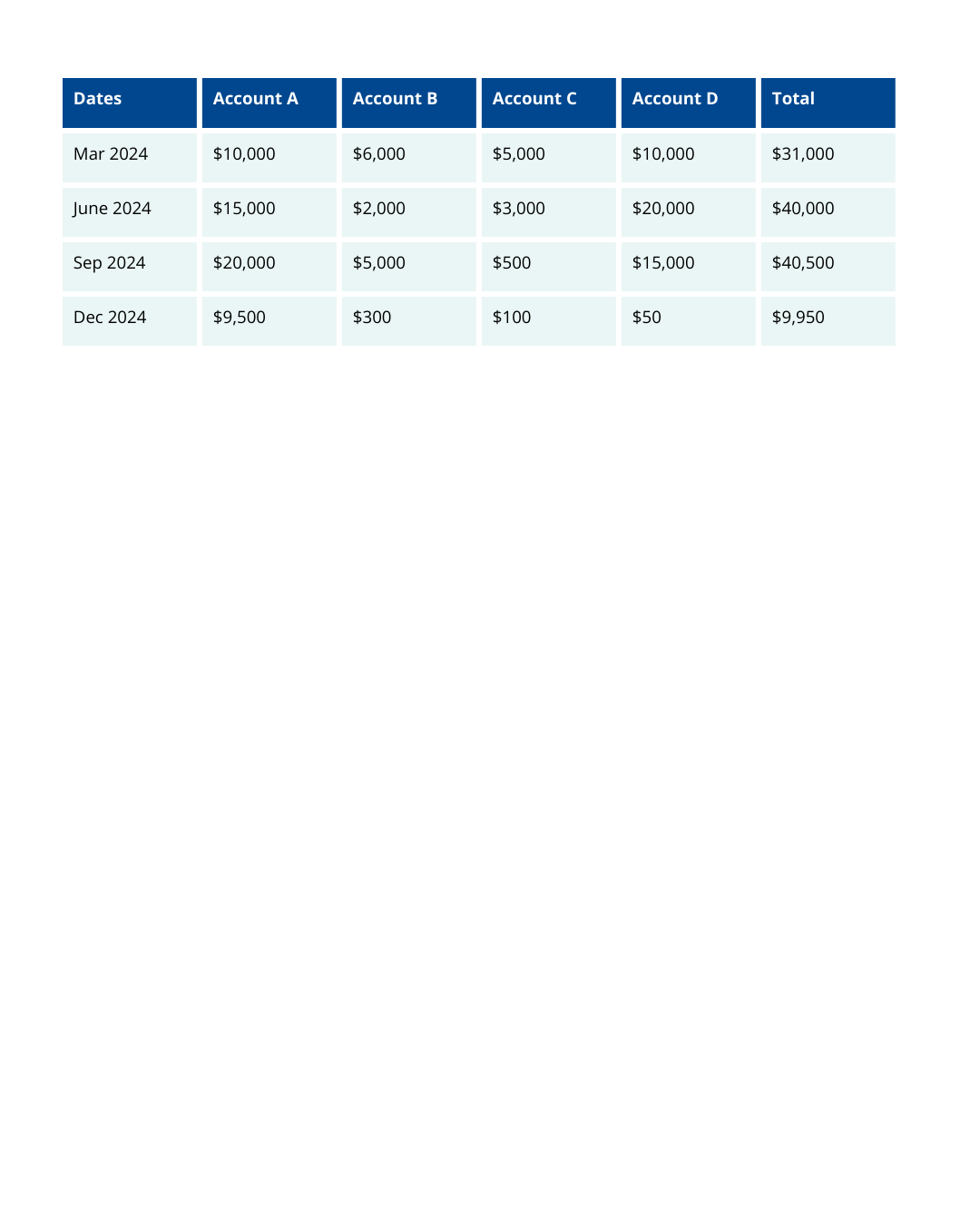

Step-by-Step Guide (Multiple Savings Account):

Determine the Nisab value in SGD for reference.

List the balances of each account according to months.

Identify the combined lowest amount from all accounts at a certain time within the Haul period (It is more accurate to calculate based on combined lowest balance at a specific point in time rather than totalling the lowest balances form each account).

Deduct any immediate debts or liabilities due within the same period (if any).

Multiply the remaining amount (lowest balance – debts) by 2.5%.

Example Calculation:

Lowest Balance: $9,950

Nisab: $9,000 (in Dec 2024)

Zakat Amount: $9,950 x 2.5% = $248.75

Tip: Use trusted tools like the MUIS Zakat Calculator for accuracy. These platforms simplify the process of Zakat calculation and ease the payment process.

3. Savings That Are Exempt from Zakat

While most forms of monetary wealth are subject to Zakat, certain exemptions exist based on specific conditions. Understanding these exemptions is essential for accurate calculations.

Common Exemptions:

Debt repayment: You can deduct immediate or within-the-year debts, such as home loan instalments or personal debt, from your Zakat-able savings.

Locked CPF or CDA funds: Zakat is not due on inaccessible assets like Child Development Account (CDA) or CPF funds. Once withdrawn, they become Zakat-able if they meet Nisab and Haul requirements.

Non-productive assets: Personal items like homes, cars, or furniture are exempt as they do not generate income (unless they are used for business purposes).

Real-Life Scenario:

If an individual has $10,000 in savings but owes $3,000 in outstanding loans that are already due, the Zakat-able savings would be $7,000. The Zakat would then be calculated only on this adjusted amount.

If an individual has $10,000 in savings and a mortgage with monthly instalments of $400, and the Zakat date coincides with the due date for the monthly payment, the Zakat-able savings would be $9,600. The Zakat would then be calculated only on this adjusted amount.

Note:

For general Singaporeans who own funds in CPF (Central Provident Fund), these funds are generally exempt from Zakat while locked in, in accordance with a MUIS fatwa. Any amount withdrawn after deducting the minimum sum, after a certain age, for personal use becomes Zakat-able once it meets the requirements of Nisab and Haul. However, there is no prohibition for individuals who choose to pay Zakat at the time of receiving the lump sum payout if they are capable of doing so. As for the monthly payouts after retirement age, Zakat is not necessary during payout as it does not meet the condition of Haul yet.

4. When and How to Pay Zakat on Savings

Zakat is due annually, based on the lunar calendar (Hijri year).

It is crucial to maintain a consistent date for Zakat calculations each year to ensure accuracy.

Many prefer to pay Zakat during Ramadan, as it coincides with the payment of Zakat Fitrah, but it can be paid at any time once the conditions are met.

Where to Fulfil Zakat Obligations in Singapore:

Zakat can be paid through authorized collection centres or the Zakat Singapore website (www.zakat.sg).

The Islamic Religious Council of Singapore (MUIS) is the authorized body responsible for the Zakat system in Singapore.

Zakat paid through authorized centres is income-deductible under the Income Tax Act.

MUIS disburses Zakat funds to the eight categories of beneficiaries (Asnaf) as stipulated in the Quran.

Alternatively, Zakat can be paid digitally through various modes, such as bank transfer, Pay Now, and online payment.

Pro Tip: Keep a record of your financial transactions throughout the year. This habit simplifies calculations and ensures no savings are overlooked.

5. The Spiritual Benefits of Paying Zakat on Savings

Zakat is more than a financial obligation; it is a means of purifying wealth and fostering personal and communal growth.

For Muslims in Singapore, Zakat plays a vital role in uplifting the community by addressing socio-economic challenges.

Impact on the Community:

In 2023, MUIS distributed $60.7 million in Zakat funds, benefiting over 31,000 individuals through assistance schemes and educational programs.

Zakat strengthens the Muslim community by supporting Asnaf categories such as the poor, the needy, and those in debt.

Spiritual Perspective:

The Prophet Muhammad (peace be upon him) said, "Charity does not decrease wealth." (Sahih Muslim). This highlights the spiritual reward of Zakat, where fulfilling this obligation increases barakah (blessings) in wealth and life.

Conclusion

Fulfilling Zakat obligations is both a personal act of worship and a communal responsibility.

By understanding what savings are subject to Zakat, how to calculate it, and where to pay it in Singapore, you can align your financial management with Islamic principles.

Zakat not only purifies your wealth but also contributes to the betterment of the Muslim community in Singapore.

Take the first step today—calculate your Zakat, ensure compliance, and make a difference in the lives of those in need.

Visit MUIS Zakat Services for more guidance and tools.

BeShariahWise

Educational Shariah screening and compliance consultation for individuals and families in Singapore.

Services

© 2026 BeShariahWise - BSW SOLUTIONS (UEN: 53506307E)

We do not provide financial advice, investment recommendations, or sell financial products.

Contact

Email: salaam@beshariahwise.com

Phone/WhatsApp: +65 9646 4283

Join our updates:

Legal & Compliance

Compliance notice

“By subscribing you agree to receive educational emails from BeShariahWise. You can unsubscribe anytime. We don’t sell or share your data.”

BeShariahWise provides educational screening and Shariah compliance consultation. We do not give financial advice, recommend specific financial products, or conduct regulated activities.

Not financial advice.

All rights reserved. Educational screening & consultation. Not financial advice.